A significant shift is underway in the global artificial intelligence landscape, revealing a nuanced picture where geographical strengths diverge across different strata of the AI technology stack. While the United States maintains a commanding lead in the development of large, foundational AI models, a new report highlights that Europe and Israel are rapidly emerging as formidable contenders, and in some aspects, even category leaders, within the crucial AI application layer. This rebalancing of power, as detailed in global venture capital firm Accel’s comprehensive 2025 Globalscape report, underscores a dynamic and increasingly competitive global AI ecosystem.

A Bifurcated AI Landscape Emerges

The Accel report, a key barometer for trends in the AI and cloud market, identifies a distinct segmentation in the global AI race. On one hand, American innovation continues to drive the frontier of large-scale AI models, characterized by their immense computational power, vast training datasets, and generalized capabilities. These foundational models, often developed by tech giants and well-funded startups in Silicon Valley and beyond, serve as the bedrock upon which specialized AI applications are built. However, the narrative changes dramatically when examining the application layer, the segment focused on delivering AI-powered solutions directly to end-users and businesses. Here, companies from Europe and Israel are demonstrating remarkable agility and attracting substantial investment, challenging the long-held perception of American technological supremacy across all AI domains.

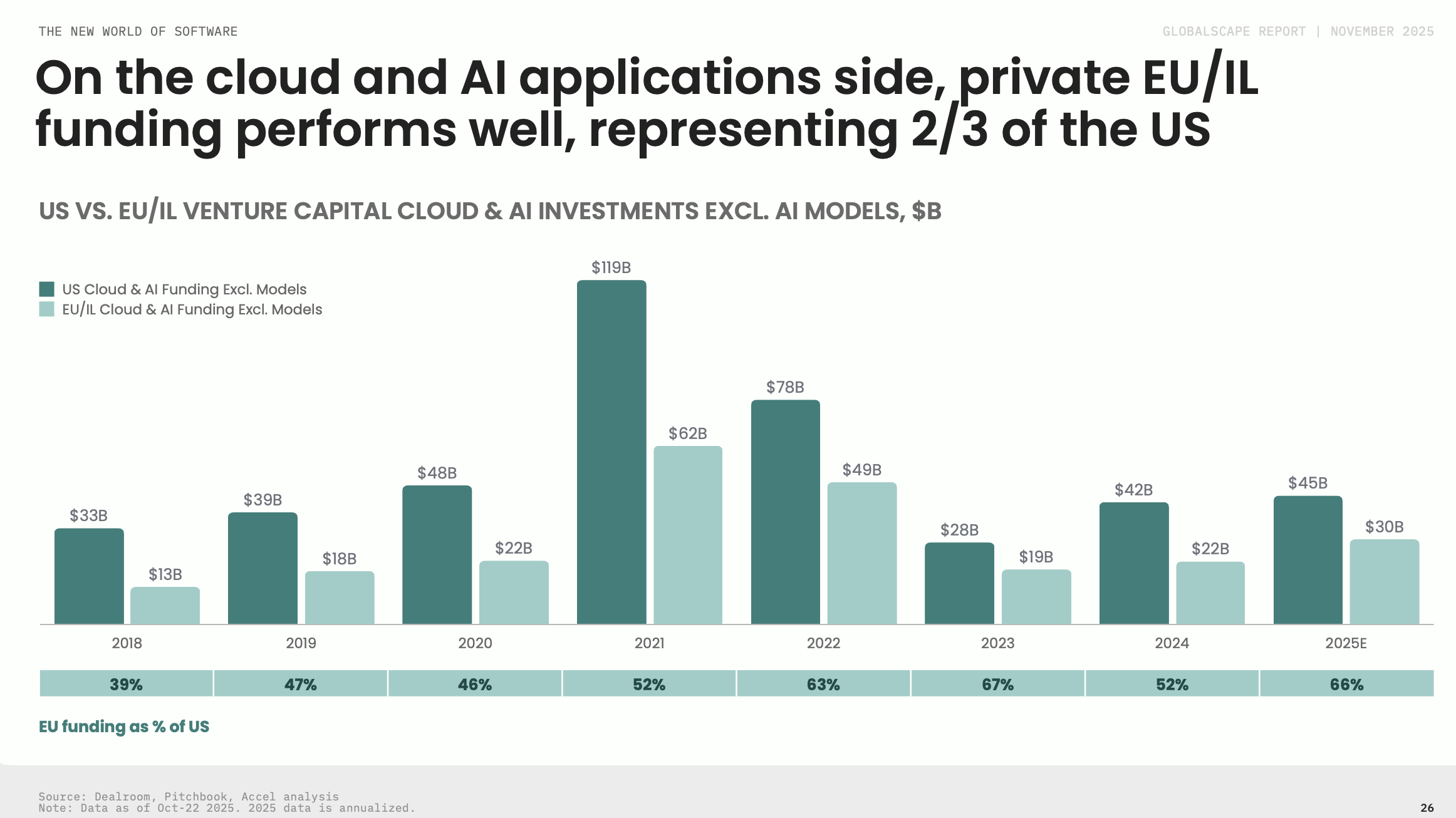

The financial metrics supporting this assertion are compelling. So far in 2025, cloud and AI applications in Europe and Israel have collectively drawn 66% as much private funding as their counterparts in the United States. This figure represents a dramatic increase from just a decade ago, when, according to Philippe Botteri, a partner at Accel, European investment in this sector was a mere tenth of what was seen in the U.S. This exponential growth in funding and innovation signifies a maturing ecosystem and a strategic pivot in how these regions are approaching the AI revolution.

The Rise of Europe and Israel: A Decade in the Making

The impressive ascent of Europe and Israel in the AI application layer is not an overnight phenomenon but the culmination of a decade-long developmental trajectory. Botteri attributes this surge to the successful cultivation of an ecosystem comprising skilled founders and savvy investors who possess a deep understanding of how to construct robust software companies. This synergistic relationship, often referred to as a "flywheel," has continuously reinforced itself, fostering a fertile ground for innovation and growth.

Background Context and Historical Trajectory

For years, European and Israeli tech ecosystems, while vibrant, often operated in the shadow of Silicon Valley. However, significant structural changes and strategic investments have propelled them forward. European Union initiatives, such as the Digital Single Market strategy and substantial research and development funding programs like Horizon Europe, have aimed to foster a continent-wide digital economy. Concurrently, national governments across Europe, from France’s "La French Tech" to Germany’s "Industrie 4.0," have poured resources into creating tech hubs, incubators, and accelerators. These efforts have been instrumental in nurturing a robust talent pool, drawing on strong traditions in STEM education and scientific research from universities like EPFL, ETH Zurich, and Cambridge.

Israel, often dubbed the "Startup Nation," has a unique history rooted in defense technology and a culture of entrepreneurial innovation. Its compulsory military service often provides young individuals with advanced technical training and experience in high-stakes environments, contributing to a dense network of skilled engineers and cybersecurity experts. This foundation has seamlessly transitioned into the civilian tech sector, making Israel a perennial hotspot for deep tech and AI innovation.

The early 2010s saw the initial blossoming of SaaS companies across Europe, demonstrating the region’s capability in enterprise software. By the late 2010s, a growing number of European startups achieved "unicorn" status, signaling increased investor confidence and market validation. This period also witnessed an acceleration in AI and machine learning research, with European institutions contributing significantly to theoretical advancements and practical applications. The current state in 2025, as revealed by Accel, is a testament to the compounding effects of these efforts, positioning Europe and Israel as significant players in the global tech arena.

Beyond capital and infrastructure, the human element is crucial. Jonathan Userovici, a Paris-based general partner at Headline, notes that founders in these regions are increasingly combining world-class technical talent with profound market expertise. This blend allows them to develop solutions that are not only technologically sophisticated but also deeply attuned to specific industry needs and pain points, whether in legal tech, healthcare, manufacturing, or marketing. This observation aligns with Headline’s own "AI Europe 100" report, which identified a curated list of AI-native application startups in Europe poised for future success, based on their growth velocity, team strength, and technological advancements.

Unprecedented Growth and Efficiency in AI-Native Applications

One of the most striking findings from the Accel report concerns the extraordinary growth velocity demonstrated by the new breed of AI-native applications. Historically, reaching $100 million in Annual Recurring Revenue (ARR) was a milestone that could take decades for a software company to achieve. However, current AI-driven applications are hitting this benchmark in a mere matter of years. This rapid scaling is profoundly impacting market entry strategies, competitive dynamics, and the overall pace of technological disruption across various sectors. Companies like Lovable and Synthesia, mentioned as emerging category leaders, exemplify this accelerated growth trajectory.

This rapid expansion is coupled with an unprecedented level of efficiency. Botteri highlights that the revenue per headcount for these AI software companies is the highest ever observed, a trend evident on both sides of the Atlantic. This remarkable efficiency is largely attributable to the very nature of AI itself. Automation, intelligent optimization, and the inherent scalability of AI tools allow these companies to deliver significant value with relatively lean teams. For businesses, this translates into lower operational costs, faster product development cycles, and the ability to serve larger customer bases without a proportional increase in human resources.

From an analytical perspective, this efficiency has significant implications for investors. Startups with high revenue per headcount are inherently more attractive, promising stronger margins and potentially faster paths to profitability. This could lead to higher valuations for AI-native companies and a reallocation of investment capital towards models that leverage AI for operational leverage. For the broader tech economy, it signals a shift in labor market demands, emphasizing roles that can design, implement, and manage AI systems rather than perform repetitive tasks.

The Enduring Role of Legacy Cloud and the AI Integration Imperative

Despite the rise of AI-native applications, the report emphasizes that "existing cloud software companies are not going away." This assertion is supported by the fact that Accel’s Public Cloud Index, which tracks the performance of publicly traded cloud companies, is up 25% year-over-year. These established players are not standing still; instead, they are actively integrating "agentic capabilities" into their existing product suites. Agentic AI refers to systems capable of understanding, reasoning, and executing tasks autonomously, often interacting with other systems or humans.

This integration strategy means that many traditional cloud software providers are effectively becoming AI-native through evolution rather than revolution. An excellent example cited is Doctolib, an Accel portfolio company based in Europe. While not born solely out of the current AI wave, Doctolib has integrated AI so deeply into its operations that it now functions as a prime example of an AI-powered enterprise. This trend underscores a crucial aspect of the current AI transition: it’s not just about entirely new companies, but also about the profound transformation of established enterprises through AI adoption. This creates a dual strategy for market players: either build AI from the ground up or infuse existing platforms with advanced AI functionalities, both leading to significant competitive advantages.

Navigating the Foundation Model Divide

While Europe and Israel demonstrate clear strengths in the application layer, the landscape for developing large, foundational AI models presents a different set of challenges. Accel’s outlook for European companies operating in this highly capital-intensive space is "less sunny," with Botteri describing it as "not a very target-rich environment." This analytical commentary reflects the immense resources required to compete with global leaders in foundational AI.

The development of large language models (LLMs) and other generative AI foundational models demands astronomical investments in computational infrastructure, access to vast proprietary datasets, and the recruitment of top-tier AI research talent. The current leaders in this domain, largely concentrated in the U.S., benefit from decades of investment in AI research within tech giants and a relatively less fragmented data environment. Companies like Mistral AI in Europe, while representing significant ambition and technical prowess, face an uphill battle against deeply entrenched and massively funded competitors.

However, this does not mean the space is entirely closed off. There remains potential for European and Israeli entities to emerge as leaders in more specialized or smaller foundational models. These could focus on specific languages, scientific domains, or industry verticals, where a smaller, highly optimized model could outperform a generalist giant. Such an approach might leverage Europe’s linguistic diversity or strong sectoral expertise. The regulatory environment, particularly the EU’s General Data Protection Regulation (GDPR), while fostering data privacy, can also present complexities for training large models on vast, diverse datasets, potentially influencing a focus on more domain-specific data and models.

The Pursuit of Defensibility and the Undervalued Data Layer

The intense competition among venture capitalists for investment opportunities in the AI application layer brings with it recurring questions about defensibility. In a rapidly evolving market, how do these AI applications build sustainable competitive advantages? For Botteri, defensibility still lies in crafting a product-centric offering that achieves fast adoption. This implies superior user experience, seamless integration, and solving critical problems more effectively than alternatives. Early market penetration and rapid user growth can create network effects, brand loyalty, and valuable feedback loops that further enhance the product.

Beyond the product itself, a growing emphasis is being placed on the underlying data. Lotan Levkowitz, a managing partner at Israeli VC firm Grove Ventures, argues that "data is undervalued at the moment." He strongly believes that companies focused on proprietary data and building "data flywheels" — systems where data collection and usage continuously improve the product, which in turn attracts more users and more data — are exceptionally lucrative.

This perspective highlights a critical future battleground in the AI space. The quality, uniqueness, and ethical sourcing of data will become increasingly important. For AI applications, proprietary datasets can act as a powerful moat, enabling superior performance and personalized experiences that are difficult for competitors to replicate. This also intertwines with social and cultural impacts, particularly concerning data privacy and ownership. Regions with strong data governance frameworks, like Europe, may find unique advantages in building trust-centric AI applications that leverage carefully curated and ethically managed datasets.

Conclusion: A Global AI Ecosystem in Flux

The global AI landscape is characterized by a fascinating interplay of specialized strengths and intense competition. While the United States continues to lead in the capital-intensive realm of large foundational AI models, the Accel Globalscape report clearly demonstrates the formidable rise of Europe and Israel in the dynamic and rapidly growing AI application layer. This shift is powered by mature tech ecosystems, a blend of deep technical and market expertise, and an unprecedented rate of growth and efficiency in AI-native solutions.

The ongoing transformation of existing cloud software companies, coupled with the strategic pursuit of defensibility through product excellence and proprietary data, indicates a multi-faceted evolution rather than a simple winner-takes-all race. As the AI stack continues to mature, from infrastructure and models to platforms and applications, the global ecosystem will likely see continued innovation, specialized competition, and strategic collaborations, ensuring that the future of artificial intelligence remains a truly international endeavor.

{kind=link}