India’s vibrant startup landscape concluded 2025 with a notable $10.5 billion in capital raised, reflecting a significant recalibration in investor sentiment and strategy. This figure, while substantial, arrived amidst a pronounced increase in selectivity, with venture capitalists and other funding entities opting for fewer, more scrutinized investments. This evolving approach marks a pivotal moment for what has rapidly become the world’s third most-funded startup market, illustrating a divergence from the highly concentrated, AI-centric capital flows observed in more mature ecosystems like the United States.

A New Chapter in India’s Startup Journey

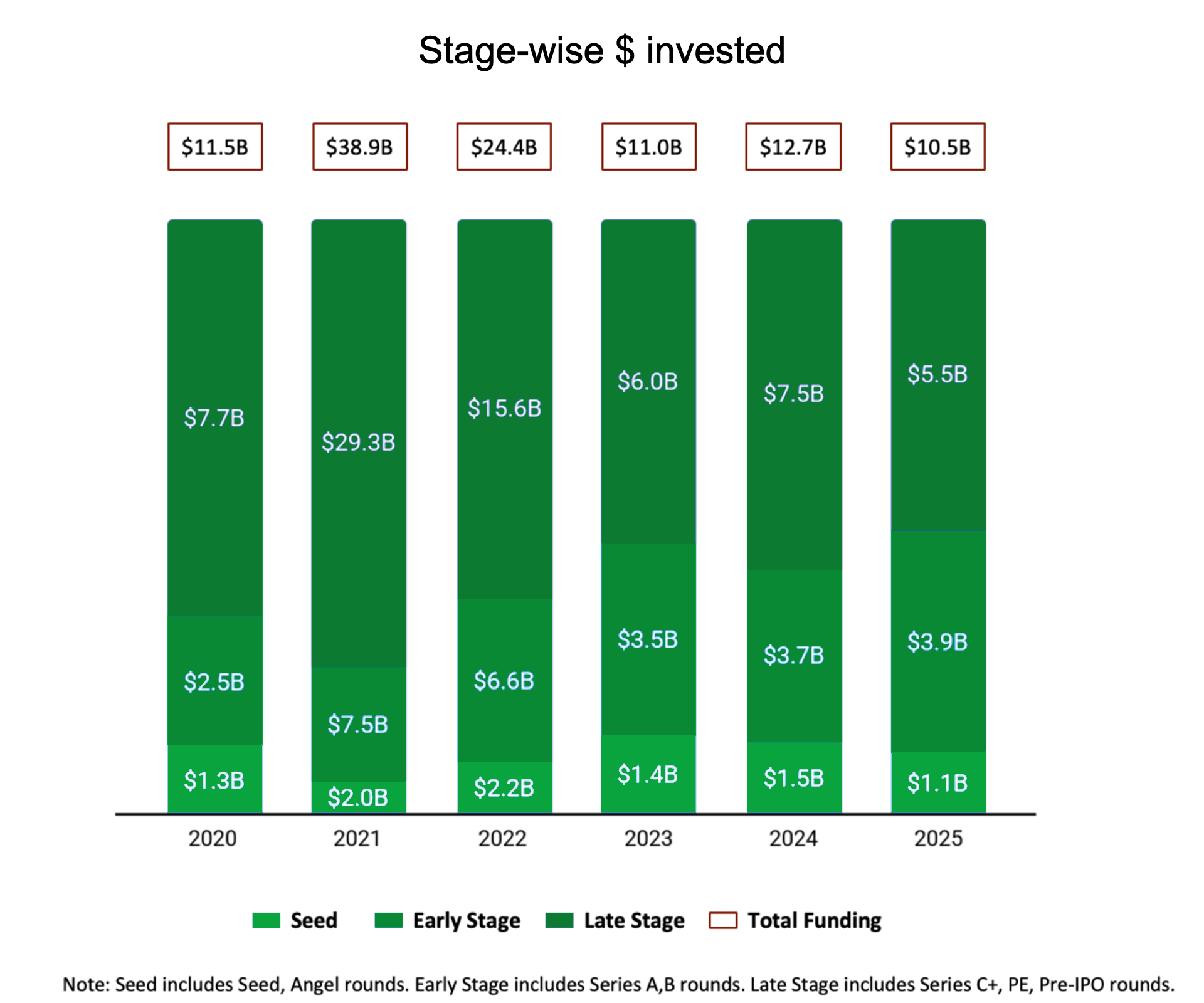

The narrative of India’s startup ecosystem has been one of explosive growth over the past decade, fueled by a burgeoning digital population, a vast talent pool, and government initiatives like ‘Startup India’ that actively foster entrepreneurial activity. The early 2020s, particularly 2021 and 2022, witnessed a funding frenzy characterized by "growth at all costs" and a rapid proliferation of unicorns. However, 2025 signaled a transition towards a more disciplined investment philosophy, influenced by global macroeconomic headwinds such as rising interest rates, inflationary pressures, and geopolitical uncertainties that have prompted a worldwide tightening of venture capital. This shift compelled investors to pivot from speculative bets to ventures demonstrating clear pathways to profitability, robust unit economics, and sustainable business models. The overall deal count starkly illustrates this cautious approach, plummeting by nearly 39% from the previous year to a total of 1,518 funding rounds, according to Tracxn data. Despite this sharp reduction in the number of deals, the total capital deployed saw a more modest decline of just over 17%, suggesting that while fewer checks were written, the average check size for successful ventures remained significant, highlighting investor confidence in a select group of high-potential companies.

Shifting Investment Dynamics Across Stages

The impact of this heightened selectivity was not uniformly distributed across all funding stages. Seed-stage funding, traditionally the breeding ground for experimental ideas, experienced a sharp contraction, falling by 30% from 2024 to $1.1 billion. This decline underscores a reduced appetite for higher-risk, unproven concepts. Similarly, late-stage funding, which typically targets established companies seeking to scale rapidly or prepare for public offerings, also cooled considerably, slipping to $5.5 billion—a 26% decrease from the previous year. This segment faced rigorous scrutiny regarding a company’s ability to demonstrate consistent growth, clear profitability metrics, and viable exit prospects.

In contrast, early-stage funding proved remarkably resilient, demonstrating a 7% year-over-year increase to reach $3.9 billion. This resilience indicates a strong and sustained interest in startups that have moved beyond the ideation phase and can showcase initial product-market fit, early revenue traction, and a compelling business model. Neha Singh, co-founder of Tracxn, commented on this trend, observing that capital deployment has increasingly focused on early-stage startups. This preference signals growing investor confidence in founders who can articulate stronger product-market fit, provide clearer revenue visibility, and demonstrate sound unit economics, particularly within a more constrained funding landscape.

India’s Measured Approach to AI Investment

The global technology narrative of 2025 was undeniably dominated by the rapid advancements and immense capital inflows into artificial intelligence. However, India’s engagement with the AI boom showcased a distinctive, more measured strategy, contrasting sharply with the AI-fueled capital concentration prevalent in the United States. In India, AI startups collectively raised just over $643 million across 100 deals during the year, representing a modest 4.1% increase from 2024. This capital was predominantly channeled into early and early-growth stage ventures, with early-stage AI funding accounting for $273.3 million and late-stage rounds attracting $260 million. This allocation reflects a clear investor preference for application-led AI businesses—solutions that leverage existing AI models to solve specific industry or consumer problems—over the capital-intensive development of foundational AI models.

This stands in stark contrast to the U.S., where AI funding in 2025 surged past an astounding $121 billion across 765 rounds, marking a 141% jump from 2024, overwhelmingly dominated by massive late-stage deals into foundational model companies. Prayank Swaroop, a partner at Accel, highlighted this disparity, noting India’s current lack of AI-first companies achieving significant revenue milestones (e.g., $40-$100 million annually) at a pace seen globally. He explained that India would require time to cultivate the necessary research depth, talent pipeline, and patient capital to compete effectively at the foundational AI layer. Consequently, focusing on application-led AI and adjacent deep-tech areas emerges as a more pragmatic and realistic strategy for the near term, leveraging India’s strengths in software services and domain expertise.

Beyond AI: Strategic Sectoral Bets

This pragmatic approach extends beyond core AI, shaping where investors are placing their longer-term bets. Venture capital is increasingly flowing into sectors like advanced manufacturing and deep-tech. These areas present a unique strategic advantage for India, as they often face less intense global capital competition compared to purely software-driven ventures. India benefits from inherent strengths in these sectors, including a growing pool of engineering talent, competitive cost structures, and unparalleled access to a vast domestic customer base.

While AI commands significant global investor attention, capital in India demonstrably remains more evenly distributed. Substantial funding continues to flow into diverse sectors such as consumer, fintech, and other deep-tech startups. Swaroop emphasized that advanced manufacturing, in particular, has emerged as a compelling long-term opportunity, witnessing a nearly tenfold increase in the number of startups over the past four to five years. He characterized this as a clear "right to win" for India, given the favorable market conditions and lower global capital competition. Rahul Taneja, a partner at Lightspeed, observed that while AI startups constituted roughly 30-40% of deals in India in 2025, there was a parallel surge in consumer-facing companies. This phenomenon is driven by the evolving behaviors of India’s urban population, which is creating robust demand for faster, more on-demand services—ranging from quick commerce to specialized household services. These categories leverage India’s unique advantages of scale and high population density, rather than requiring the hyper-capital intensity often associated with Silicon Valley models.

Divergent Paths: India Versus the U.S.

Data from PitchBook starkly illustrates the divergence in capital deployment between India and the U.S. in 2025. U.S. venture funding experienced a massive surge, reaching $89.4 billion in the fourth quarter alone (up to December 23), whereas Indian startups collectively raised approximately $4.2 billion during the same period. However, Taneja of Lightspeed cautioned against simplistic direct comparisons between the two ecosystems. He argued that fundamental differences in population density, labor costs, and consumer behavior profoundly influence which business models can achieve scalable success. Categories like quick commerce and on-demand services, for instance, have found significantly greater traction and market fit in India than in the U.S., reflecting distinct local economic realities rather than any perceived lack of ambition among Indian founders or investors.

Lightspeed’s global strategy, which recently saw the firm raise a record $9 billion in fresh capital with a strong focus on AI, does not signal a wholesale shift in its India approach. Taneja clarified that the global fund is tailored for a different market and maturity cycle. Lightspeed’s India arm will continue its established strategy of backing promising consumer startups while selectively exploring AI opportunities that are specifically shaped by local demand and avoid the global capital intensity required for foundational model development.

Fostering Inclusivity and Local Participation

Amidst the broader funding shifts, India’s startup ecosystem also saw specific segments face tighter capital conditions. Funding for women-led startups, for instance, held relatively steady at approximately $1 billion in 2025, experiencing a modest 3% decline from the previous year, according to Tracxn’s report. However, this headline figure belied a more significant pullback beneath the surface: the number of funding rounds for women-founded startups plummeted by 40%, and the number of first-time funded women-led ventures decreased by 36%. This highlights persistent challenges in ensuring equitable access to early-stage capital and maintaining momentum for diverse founders.

Overall investor participation narrowed sharply as selectivity intensified. Approximately 3,170 investors engaged in funding rounds in India in 2025, a substantial 53% drop from roughly 6,800 investors a year earlier. Intriguingly, India-based investors accounted for nearly half of this activity, with around 1,500 domestic funds and angels participating. This trend suggests that local capital played an increasingly prominent and stabilizing role as global investors adopted a more cautious stance. Activity also became more concentrated among a smaller group of repeat backers, with Inflection Point Ventures leading the pack, participating in 36 funding rounds, closely followed by Accel with 34, according to Tracxn data.

Government Catalysis and De-Risking the Ecosystem

The Indian government’s proactive involvement in the startup ecosystem became significantly more visible and impactful in 2025. New Delhi initiated a $1.15 billion Fund of Funds in January, designed to expand capital access for startups across various stages. This was swiftly followed by a monumental ₹1 trillion ($12 billion) Research, Development, and Innovation scheme. This ambitious initiative targeted strategic areas such as energy transition, quantum computing, robotics, space technology, biotechnology, and artificial intelligence, employing a mix of long-term loans, equity infusions, and direct allocations to deep-tech funds.

This robust governmental push has successfully catalyzed private capital. The government’s increasing engagement helped spur a nearly $2 billion commitment from prominent U.S. and Indian venture capital and private equity firms, including Accel, Blume Ventures, and Celesta Capital, specifically aimed at backing deep-tech startups. This collaborative effort also brought industry giants like Nvidia onboard as an adviser and attracted investments from Qualcomm Ventures. Furthermore, in a rare federal intervention, the Indian government co-led a $32 million funding round for quantum computing startup QpiAI earlier in the year, underscoring its strategic commitment to emerging technologies.

This growing state involvement has been instrumental in alleviating a critical concern long flagged by investors: regulatory uncertainty. Taneja of Lightspeed noted that one of the biggest risks investors are reluctant to underwrite is the potential for sudden regulatory shifts. As government entities become more familiar with the intricacies of the startup ecosystem and actively participate in its growth, policy frameworks are more likely to evolve in alignment with industry needs, thereby reducing uncertainty for investors backing companies with longer development cycles and higher capital requirements.

Maturing Exit Avenues and Unicorn Dynamics

The reduced regulatory uncertainty and a more disciplined approach to investment have begun to manifest positively in India’s exit markets. The country saw a consistent pipeline of technology initial public offerings (IPOs) over the past two years, with 42 tech companies going public in 2025, a 17% increase from 36 in 2024, according to Tracxn. Crucially, a significant portion of the demand for these listings originated from domestic institutional and retail investors. This development addresses a long-standing concern that Indian startup exits were overly reliant on volatile foreign capital, especially during periods of global economic instability. M&A activity also picked up pace, with acquisitions rising 7% year-over-year to 136 deals, Tracxn data indicates.

Accel’s Swaroop confirmed that earlier investor worries about the sustainability of India’s public markets, particularly their dependence on foreign capital during global downturns, have largely been disproven this year. He pointed to the growing role of domestic investors in absorbing technology listings as a significant shift that has made exits more predictable and reduced reliance on often-unpredictable overseas flows.

India’s unicorn pipeline in 2025 further reflected this overarching shift toward restraint and efficiency. While the number of new unicorns remained flat year-over-year, Indian startups achieved $1 billion valuations with less capital, fewer funding rounds, and from a smaller pool of institutional investors. This trend signifies a more measured and capital-efficient path to scale compared to both previous boom years and global peers, indicating a maturing ecosystem where valuations are increasingly tied to demonstrable value and sustainable growth.

Looking Ahead: Resilience and Strategic Growth

As India transitions into 2026, challenges persist, particularly concerning its positioning in the global race for AI leadership and the need to deepen its late-stage funding environment without succumbing to the pressures of outsized capital inflows. Nevertheless, the profound shifts observed in 2025 signal an Indian startup ecosystem that is not merely enduring but actively maturing. Capital is now being deployed with greater deliberation, exit opportunities are becoming more predictable and domestically driven, and the unique dynamics of the local market are increasingly shaping its growth trajectory. For investors, India is evolving beyond being merely an alternative to developed markets; it is emerging as a complementary arena with its own distinct risk profile, investment timelines, and a wealth of unique opportunities, underscored by its growing self-reliance and strategic focus.

{kind=link}