The personal computing market in India achieved an unprecedented milestone in 2025, recording its most robust performance to date and significantly outpacing the surge in demand observed during the COVID-19 pandemic. This remarkable growth was predominantly fueled by a substantial wave of first-time buyers, who initially acquired devices during the lockdown periods and are now transitioning to upgraded models.

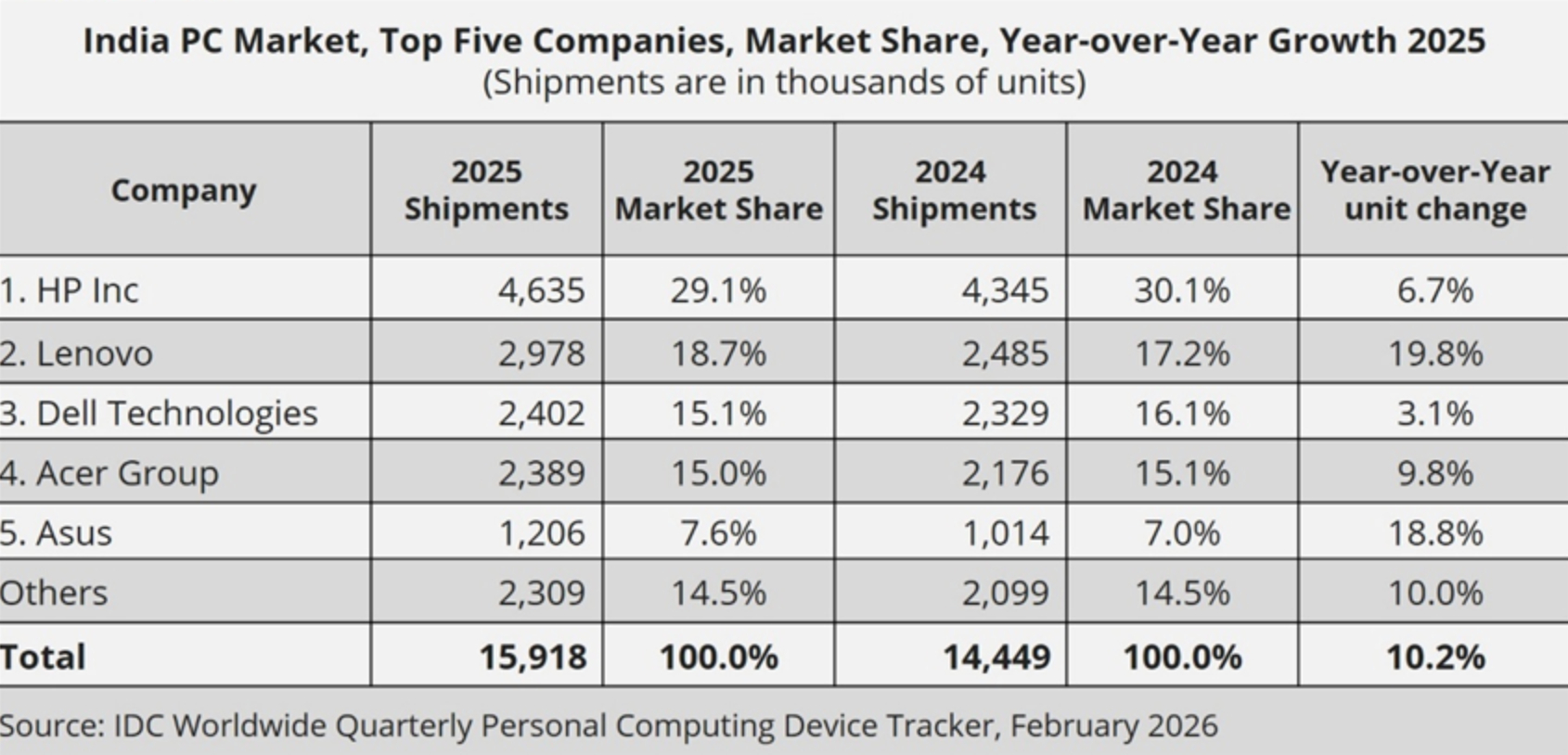

According to detailed analysis from IDC, shipments of desktops, notebooks, and workstations across India experienced a notable 10.2% year-over-year increase, culminating in a total of 15.9 million units shipped throughout 2025. This figure not only represents the first instance of annual shipments surpassing the 15-million-unit threshold but also comfortably exceeds the previous peaks established in 2021 and 2022, signaling a sustained and deepening embrace of personal computing within the nation.

A New Digital Horizon for India

India, a nation characterized by its immense population and rapidly expanding economy, has long been on a trajectory of digital transformation. For many years, the primary gateway to the internet and digital services for the average Indian consumer was the mobile phone, specifically smartphones. This mobile-first approach was largely a function of affordability and accessibility, with feature phones giving way to increasingly sophisticated and inexpensive smartphones that allowed millions to access online content, communication, and services for the first time. Government initiatives like "Digital India," launched in 2015, have further accelerated this transformation, aiming to improve online infrastructure, enhance digital literacy, and make government services available electronically.

Despite the mobile revolution, PC penetration in India remained relatively low compared to developed economies. Before the pandemic, many households and small businesses considered personal computers a luxury rather than a necessity. The landscape, however, began to shift dramatically with the onset of global health crises, fundamentally altering how work, education, and commerce were conducted.

The Pandemic’s Catalytic Role and Subsequent Growth

The global health crisis that began in 2020 served as an unforeseen catalyst for India’s PC market. As stringent lockdowns were implemented to curb the spread of the virus, remote work became the norm for professionals, and online learning quickly replaced traditional classroom instruction for students across all age groups. This sudden and widespread shift exposed a significant portion of the Indian population to personal computers for the very first time. Families that previously managed with a single shared device or relied solely on smartphones found themselves needing dedicated machines for work, school, and even entertainment. This created an immediate and unprecedented surge in demand for laptops and desktops, as households scrambled to equip themselves for the new digital reality.

This initial wave of purchases in 2020-2022 laid the foundation for the current market boom. As these first-generation pandemic-era devices naturally age, typically within a 3-5 year lifespan, a substantial segment of users is now entering an upgrade cycle. This phenomenon is a critical driver of the record-breaking shipments witnessed in 2025. What started as a reactive necessity has evolved into an established dependency, with users now more aware of the benefits of faster processors, larger storage, and improved ergonomics offered by newer models.

Drivers of the Unprecedented Surge

Beyond the natural upgrade cycle, several other macro and micro factors are contributing to India’s robust PC market performance. Growing digitization efforts across various sectors continue to stimulate demand. Businesses of all sizes, from nascent startups to established small and medium-sized enterprises (SMBs), are increasingly adopting personal computers to streamline operations, manage data, and engage with clients in an ever-more digital economy. This institutional shift towards digital workflows necessitates a broader and more sophisticated IT infrastructure.

Furthermore, the increased availability of devices, coupled with improved distribution networks, has expanded the reach of personal computing beyond India’s traditional metropolitan hubs. Smaller cities and semi-urban areas, which were previously underserved, are now becoming significant growth engines. This decentralization of demand reflects a broader trend of economic and digital empowerment spreading across the country, as internet access becomes more pervasive and affordable, encouraging more individuals and businesses to invest in essential computing tools. This wider geographical penetration is key to unlocking the vast untapped potential of the Indian market.

The global context also underscores India’s unique position. While worldwide PC shipments collectively expanded by 8.1% to 284.7 million units in 2025, India’s contribution to this global figure has grown disproportionately. Its share of global PC shipments rose significantly to 5.6% in 2025, a notable increase from just 3.3% in 2020. This trend firmly establishes India as one of the fastest-growing personal computing markets globally, demonstrating its pivotal role in the future of the technology industry.

Commercial and Consumer Dynamics

The Indian PC market’s strength in 2025 was a result of robust demand from both commercial and consumer segments. Commercial buyers constituted a larger share, accounting for 52.9% of total PC shipments, while the consumer segment made up the remaining 47.1%.

The commercial segment’s impetus stemmed from several factors. A significant driver was the ongoing Windows refresh cycle, where many enterprises opted to upgrade their operating systems and hardware. This cycle is typically driven by the need for enhanced security, improved performance, and compatibility with newer software applications, especially as older Windows versions approach their end-of-life support. Additionally, a substantial number of small and medium-sized businesses, alongside various public sector organizations, have embarked on initiatives to replace their aging fleets of devices, further bolstering commercial demand. This systemic modernization within organizations reflects a broader recognition of the strategic importance of up-to-date technology for productivity and competitiveness.

The consumer segment, on the other hand, was largely driven by the upgrade phenomenon among those who purchased their first PCs during the pandemic. As digital literacy increases and the use cases for personal computers expand beyond basic tasks to include content creation, advanced gaming, and sophisticated online learning, consumers are seeking more powerful and feature-rich devices. The aspiration for better technology, combined with increased disposable income in certain demographics, continues to fuel this part of the market.

Vendor Landscape and Competitive Strategies

The competitive landscape in the Indian PC market is dynamic, with several major players vying for market dominance. Traditional global giants such as HP, Lenovo, Dell, Acer, and Asus emerged as the leading PC vendors in India during the past year. These companies have established extensive distribution networks, diverse product portfolios catering to various price points, and robust after-sales service infrastructure, all crucial for success in a diverse and price-sensitive market like India.

Apple’s Mac computers, while globally recognized for their premium quality and user experience, hold a comparatively smaller slice of India’s personal computing market. In 2025, MacBooks accounted for approximately 5.6% of India’s notebook market. This contrasts sharply with their global share, which typically hovers between 11% and 12%, and their significant presence in the U.S. market, where they command around 20%. Historically, MacBooks’ share in India’s notebook market did see an increase, peaking at 7.4% in 2022 from 3.9% in 2020, indicating a growing but still niche appeal.

A significant reason for Apple’s relatively lower market share lies in its premium pricing strategy, which can be a barrier in a market where affordability often dictates purchasing decisions. Furthermore, Apple’s presence in the enterprise segment within India is limited, with an estimated 85% to 87% of Mac shipments originating from the consumer segment. However, strategic shifts are underway. The introduction of lower-priced models, such as the recently launched MacBook Neo, alongside a perceived increase in the cost of Windows notebooks, could potentially make Apple products more accessible to a wider Indian audience. Moreover, Apple’s reported focus on expanding its footprint in the commercial segment could be a significant growth vector, allowing the company to tap into the burgeoning enterprise and SMB demand.

The Evolving Role of Premium Devices and AI

The premium notebook segment, defined by devices priced above $1,000, also demonstrated healthy growth, expanding by 8.2% year-over-year in 2025. This indicates a steady demand for higher-end devices, suggesting an increasing willingness among certain consumer and commercial buyers to invest in more capable and durable computing solutions. This trend is particularly relevant as advanced features, including artificial intelligence (AI) capabilities, begin to integrate into premium laptops.

While AI features are still in their nascent stages and not yet a primary driver of overall PC demand in India, their influence is growing. Many enterprises that previously invested in high-end notebooks are now finding that AI-enabled PCs fall within similar budget ranges, making them an attractive upgrade. For sectors heavily reliant on data processing, analytics, and automation, AI PCs offer significant advantages in efficiency and capability. Furthermore, the burgeoning community of digital content creators in India, driven by the nation’s rising digital media consumption, is also expected to contribute to the adoption of AI-powered devices, leveraging their enhanced processing power for tasks like video editing, graphic design, and complex rendering. The long-term impact of AI integration is expected to be substantial, reshaping user expectations and application development.

Navigating Future Challenges and Opportunities

Despite the exceptional performance in 2025, the Indian PC market is not immune to potential headwinds in the immediate future. Rising component prices and persistent global supply chain challenges could exert pressure on demand, potentially leading to a moderation in growth. Analysts project that PC shipments in India could experience a modest decline of approximately 5% in 2026, though this is still a more optimistic outlook compared to the low double-digit drop anticipated for the global market.

India’s resilience in the face of these challenges is attributed to its fundamental market characteristics. The country’s relatively low PC penetration, estimated at around 17% to 20%, signifies a vast untapped market with considerable room for expansion. This structural advantage, combined with the sheer scale of its population and ongoing digital adoption across households and businesses, positions India to outperform many other markets.

Long-Term Outlook: India’s Digital Trajectory

The market is expected to remain under some pressure into 2027 as it absorbs the current economic and supply chain dynamics. However, a return to robust growth is anticipated thereafter, as demand from both businesses and consumers stabilizes and new technological innovations, such as more pervasive AI integration and evolving form factors, stimulate further upgrades and new purchases.

The long-term trajectory for India’s personal computing market remains overwhelmingly positive. As the nation continues its ambitious digital transformation journey, fueled by government initiatives, a young and digitally-native population, and a rapidly evolving economic landscape, the PC will remain a crucial tool for productivity, education, and entertainment. The current record-breaking performance is not merely a transient surge but rather a strong indicator of India’s deepening commitment to digital empowerment and its increasing prominence on the global technology stage.

{kind=link}