The landscape of autonomous transportation is undergoing a significant transformation, marked by Waymo’s strategic expansion of its commercial robotaxi service onto the intricate network of freeways across major U.S. metropolitan areas. While routine announcements of new city launches often capture headlines, industry analysts are increasingly highlighting the integration of high-speed arterial roads as a pivotal advancement, fundamentally altering the operational scope and economic viability of self-driving fleets. This move, now commercially active in the San Francisco Bay Area, Phoenix, and Los Angeles, represents a crucial step in fulfilling the long-held promise of seamless, efficient autonomous travel.

The Freeway Frontier: Waymo’s Strategic Expansion

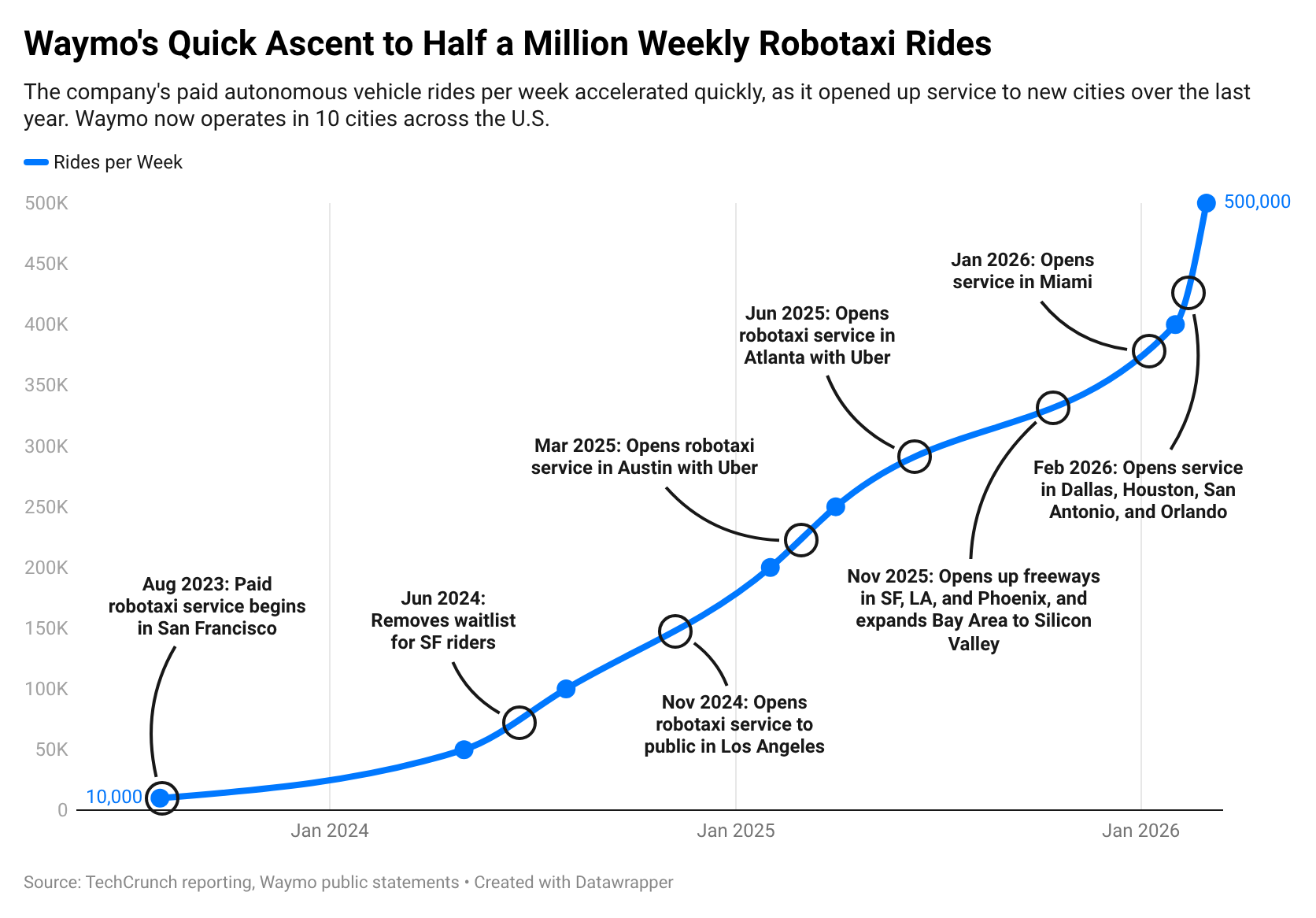

Waymo, originally conceived as the Google self-driving car project in 2009, has long been at the forefront of autonomous vehicle (AV) development. Its journey began with extensive research and development under Google X, evolving into an independent Alphabet subsidiary in 2016. The company’s methodical, safety-first approach has seen its vehicles accumulate millions of miles in real-world conditions, gradually transitioning from research prototypes to commercial robotaxi services. Initial deployments focused on geo-fenced urban areas, meticulously mapping and understanding complex city streets, intersections, and pedestrian behaviors. The move to freeways, however, signifies a new chapter, addressing a distinct set of technical and logistical challenges.

Navigating freeways presents a significantly different operational environment compared to urban streets. Higher speeds, rapid lane changes, intricate merge points, sudden debris, and the dynamic behavior of human drivers demand an elevated level of perception, prediction, and control from autonomous systems. Waymo’s years of testing and refinement in these demanding conditions have culminated in this commercial rollout, demonstrating a maturation of its underlying technology. This strategic shift is not merely about increasing square mileage; it’s about unlocking the connective tissue that links sprawling metropolitan areas. For regions like the San Francisco Bay Area, this expansion encompasses a vast 260-square-mile zone, integrating Silicon Valley with the urban core of San Francisco and its surrounding communities.

The immediate impact for consumers is tangible. Waymo has indicated that utilizing freeways can reduce ride times by as much as 50%, a significant improvement in efficiency that enhances the appeal of robotaxi services, especially in congested areas. Moreover, freeway access is indispensable for one of the most coveted and economically significant routes: airport transfers. The company is actively testing routes to and from San Francisco International Airport (SFO), a service that, once fully commercialized, could represent a major "unlock" for its business model. Airports are high-demand hubs, offering consistent ridership and often commanding premium fares, making them critical for achieving profitability in the capital-intensive autonomous mobility sector.

However, the path to profitability for robotaxi operators remains a subject of intense scrutiny and analytical commentary. Developing and deploying autonomous technology requires colossal investments in research, hardware, software, regulatory compliance, and operational infrastructure. While increased efficiency and expanded service areas are positive indicators, the overall economics depend on factors like vehicle utilization rates, maintenance costs, charging infrastructure, regulatory fees, and pricing strategies. Until detailed balance sheets are made public, the long-term financial viability of these ambitious expansions will continue to be debated. Nevertheless, the ability to offer faster, more direct routes, especially to critical locations like airports, undeniably strengthens Waymo’s competitive position against traditional ride-hailing services and other emerging AV players.

Investment and Market Dynamics in Advanced Mobility

The broader advanced mobility sector continues to attract significant investment, albeit with evolving market sentiments. Special Purpose Acquisition Company (SPAC) mergers, while perhaps not experiencing the boom of a few years prior, remain a pathway for autonomous vehicle companies seeking public market access. Einride, the Swedish startup specializing in electric and autonomous trucks, exemplifies this trend with its plan to go public via a SPAC merger valuing the company at $1.8 billion. This move comes shortly after a $100 million private funding round. Einride’s strategy is notable because it already generates revenue, primarily from its software-as-a-service offerings and a fleet of 200 heavy-duty electric trucks deployed with major clients like Heineken and PepsiCo. This revenue stream distinguishes it from many pre-revenue transportation companies that sought SPAC listings, offering a more tangible business foundation as its distinctive autonomous pod-like trucks continue pilot operations. The merger is anticipated to finalize in the first half of 2026, marking its debut on the New York Stock Exchange.

Beyond SPACs, a diverse array of companies across the mobility spectrum secured substantial funding:

- Forterra, a developer of autonomous technology for defense applications, raised an impressive $238 million in equity and debt funding. This highlights the growing convergence of autonomous tech with national security interests.

- Gopuff, the rapid-delivery pioneer, secured $250 million in a funding round, though this came with a notable valuation markdown to $8.5 billion from its previous highs in 2021. This reflects the recalibration of valuations in the "instant commerce" sector amid increasing scrutiny of profitability.

- Harbinger, a Los Angeles-based electric truck startup, raised $160 million in a Series C round, co-led by FedEx. As part of this strategic investment, FedEx placed an order for 53 of Harbinger’s electric truck chassis, signaling a strong corporate commitment to electrifying logistics fleets.

- Octopus Electric Vehicles, a prominent UK-based EV leasing business, significantly expanded its funding lines to £2 billion ($2.6 billion) through agreements with major lenders. This underscores the robust demand for EV financing solutions as the transition to electric transportation accelerates.

- Teradar, a Boston-based startup, emerged from stealth with $150 million in Series B funding for its solid-state sensor technology. Specializing in all-weather sensing, Teradar addresses a critical need for robust perception systems in autonomous vehicles, capable of operating reliably in diverse environmental conditions.

- Upway, an e-bike refurbishment startup, raised $60 million in Series C funding, bringing its total capital raised to over $125 million since its 2021 founding. This signals the increasing importance of circular economy models in micro-mobility.

- Vay, a German startup pioneering remote-piloted rental cars, secured a $60 million investment from Singaporean tech giant Grab, with potential for an additional $350 million based on performance milestones. Remote driving offers a unique operational model, potentially bridging the gap to full autonomy or serving niche applications.

These varied funding rounds demonstrate continued investor confidence in the long-term potential of advanced mobility, even as market dynamics prompt more disciplined evaluations of business models and paths to profitability.

Leadership Transitions and Corporate Maneuvers

In the competitive luxury electric vehicle market, Lucid Motors is reportedly nearing a decision on its next permanent CEO. The search has been ongoing for approximately nine months since Peter Rawlinson’s unexpected resignation. Industry sources suggest an external candidate is favored, which would likely see interim CEO Marc Winterhoff return to his Chief Operating Officer role. This leadership change comes at a critical juncture for Lucid, as it navigates production ramp-ups, intense competition from established luxury brands and Tesla, and the broader challenges facing EV startups in securing market share and achieving scale.

Evolving Landscape of Electric Vehicles

The push towards electrification extends across the automotive industry, encompassing both legacy automakers and new entrants. Ford is expanding its BlueCruise hands-free highway driving technology into Europe, making it available on several popular models starting in spring 2026. This move reflects the global demand for advanced driver-assistance systems (ADAS) and Ford’s commitment to integrating such features into its international product lineup.

Toyota has made a significant commitment to domestic EV battery production, commencing operations at its new $13.9 billion battery plant in North Carolina. This facility, the automaker’s first battery plant outside Japan, is part of a broader strategy to localize its EV supply chain and reduce reliance on overseas manufacturing. Toyota also announced plans to invest an additional $10 billion in the U.S. over the next five years, underscoring the strategic importance of North America in its global electrification roadmap.

Conversely, some segments of the EV market are facing headwinds. Rad Power Bikes, a prominent e-bike manufacturer, has reportedly informed employees of a potential shutdown in January if new funding or an acquisition cannot be secured. This situation highlights the challenges faced by hardware-focused startups, often grappling with supply chain complexities, intense competition, and a tougher funding environment for capital-intensive ventures.

Diverse Innovations and Industry Challenges

Innovation continues across various mobility domains. Joby Aviation conducted the inaugural flight of its turbine-electric, autonomous VTOL aircraft, a demonstrator built on its electric air taxi platform but designed for defense applications. This showcases the versatility of electric vertical takeoff and landing (eVTOL) technology beyond urban air mobility.

The ride-hailing sector is also evolving. Lyft has partnered with Curb, a platform for licensed taxis, to integrate Curb’s network of drivers into the Lyft app, starting in Los Angeles. This collaboration aims to enhance ride efficiency and provide more opportunities for traditional taxi drivers, potentially addressing driver supply challenges and offering more immediate ride options for consumers. Uber, meanwhile, is piloting in-app video recording for drivers in India, a measure likely aimed at enhancing safety and accountability. The company is also expanding its premium offerings with initiatives like "Uber Ski," allowing advanced reservations for trips to major ski resorts in North America and Europe, catering to specialized travel needs.

In the realm of transit technology, Via, a publicly traded transit software company, reported a net loss of $36.9 million in its first earnings report since going public, despite an 11% year-over-year revenue increase to $713 million. This performance underscores the challenges of achieving profitability in the Mobility-as-a-Service (MaaS) sector, which often involves complex partnerships with public transit agencies and optimizing demand-responsive systems.

Finally, Tesla, a perennial subject of industry discussion, faced a mix of developments. Persistent calls for Apple CarPlay integration in its vehicles continue, while the company grappled with an expanded recall of its Powerwall 2 energy storage product due to fire reports. Furthermore, The Boring Company, another Elon Musk venture, faced scrutiny following reports of chemical burns sustained by firefighters during a safety drill at a Las Vegas construction site, adding to a history of controversy surrounding its tunnel excavation projects. The company’s ambitious product goals, such as delivering 20 million vehicles or deploying 1 million robotaxis by 2035, remain highly debated, with a recent poll indicating a significant split between those who believe Tesla will achieve its vehicle delivery target and those who doubt any of its stated long-term goals will be met.

The dynamic and multifaceted nature of the mobility industry continues to present both immense opportunities and significant hurdles. Waymo’s freeway expansion represents a crucial technical and strategic leap, potentially accelerating the widespread adoption of robotaxis. However, the diverse challenges faced by companies across the sector – from funding and profitability to regulatory compliance and public perception – underscore that the journey toward a fully autonomous and electrified transportation future is a complex, ongoing evolution.

{kind=link}