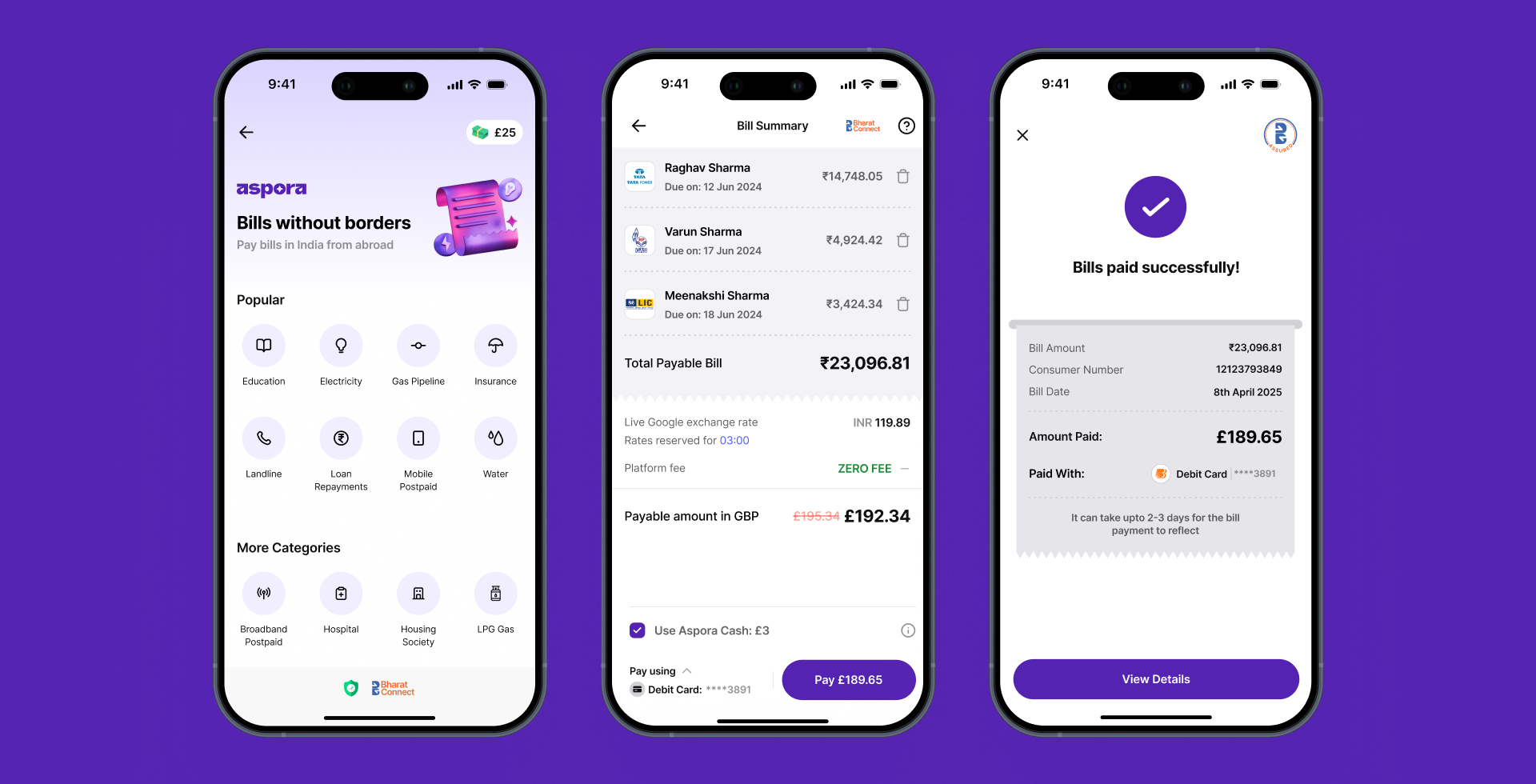

A significant advancement in cross-border financial services is set to redefine how the Indian diaspora manages financial commitments back home. Aspora, a burgeoning fintech platform backed by prominent investors like Sequoia, has introduced an innovative feature allowing non-resident Indians (NRIs) to directly pay utility bills and recharge mobile prepaid plans for their families in India. This new functionality addresses a long-standing pain point for millions living overseas, transforming what was once a cumbersome process into a seamless digital experience.

The Evolving Landscape of Diaspora Finance

The Indian diaspora is one of the largest and most economically significant in the world, with an estimated 32 million people residing outside India. Their financial contributions to their home country are immense, making India consistently the top recipient of remittances globally. In 2023, India received over $125 billion in remittances, according to the World Bank, a testament to the strong economic and cultural ties that bind NRIs to their homeland. Historically, managing finances across borders has presented numerous challenges, often characterized by complex procedures, high transaction costs, and significant delays.

For generations, NRIs have navigated a labyrinth of options to support their families in India. The most common methods involved traditional bank transfers, often incurring substantial fees and unfavorable exchange rates, or relying on informal channels which, while sometimes faster, lacked the security and transparency of regulated services. As digital technology advanced, specialized money transfer operators emerged, offering slightly improved efficiency. However, even these services primarily focused on person-to-person cash transfers, leaving the critical task of bill payments to either the recipient in India or requiring the NRI to initiate a separate, often convoluted, process. This usually meant transferring funds to an Indian account first, then coordinating with family members to ensure bills were paid on time, or attempting to use international cards on Indian payment portals, frequently encountering high foreign transaction fees and frustrating payment failures due to regional restrictions. This new offering from Aspora represents a crucial evolution, moving beyond simple money transfers to direct financial utility management.

Aspora’s Direct Payment Innovation

Aspora’s latest feature directly tackles these inefficiencies by integrating with India’s robust digital payment infrastructure. The platform has established a connection to the Bharat Bill Payment System (BBPS) through Yes Bank’s domestic pipeline. This strategic integration enables Aspora to facilitate payments for an extensive network of over 22,000 billers across India. The range of services covered is comprehensive, encompassing essential utilities such as electricity providers like BSES and BESCOM, major broadband and telecom services including Jio and Airtel, and even loan payments for leading banks.

A significant competitive advantage highlighted by Aspora is its commitment to transparency and affordability. The company states it will not charge any additional fees for these bill payments, and users will benefit from optimal exchange rates when paying directly in foreign currency. This approach not only alleviates the financial burden on NRIs but also ensures that the maximum value of their hard-earned money reaches its intended purpose without erosion from intermediary charges. Parth Garg, Aspora’s founder and CEO, emphasized the transformative nature of this solution, stating, "For millions of Indians living overseas, paying bills in India has always been unnecessarily complex – involving transfers, delays, and double fees. Aspora has now solved this large-scale problem at the tap of a button." This sentiment underscores the company’s ambition to simplify a critical aspect of cross-border financial interactions.

The Backbone: India’s Digital Payment Revolution and BBPS

The success and scalability of Aspora’s new feature are intrinsically linked to the monumental strides India has made in digital payments over the past decade. The Indian government and the Reserve Bank of India (RBI) have actively promoted a cashless economy, leading to the development of world-class digital payment infrastructures. Key among these is the Unified Payments Interface (UPI), which has revolutionized real-time peer-to-peer and merchant payments within India. Complementing UPI, the Bharat Bill Payment System (BBPS) was conceptualized and implemented by the National Payments Corporation of India (NPCI) as an integrated bill payment system offering interoperable and accessible bill payment services to customers across the country.

Launched in 2016, BBPS aimed to streamline recurring bill payments for electricity, water, gas, telecom, DTH, and more, under a single platform. It created an ecosystem where customers could pay bills anytime, anywhere, through multiple channels (online, mobile app, agent outlets) with instant confirmation. By standardizing the bill payment process, BBPS brought transparency, reliability, and convenience to millions of Indian consumers. For fintech platforms like Aspora, integration with BBPS is a game-changer, providing a single gateway to a vast network of billers without needing individual agreements with each. This robust digital public infrastructure significantly lowers the barrier to entry for innovative financial services, enabling them to offer sophisticated solutions to both domestic and international users.

Strategic Alliances and Expanding Horizons

While BBPS covers a broad spectrum of bill payments, certain categories, such as international mobile recharges and specific credit card payments for foreign payers, fall outside its current scope. Recognizing this gap, Aspora has forged a partnership with Ding, a leading international mobile recharge company. This collaboration ensures that users can also top up mobile prepaid plans for their families in India seamlessly through the Aspora platform, covering virtually all essential recurring expenses. This demonstrates a comprehensive approach to solving the diaspora’s financial needs, not just relying on existing infrastructure but also building out capabilities where needed.

The rollout strategy for this new feature is carefully phased. Currently available to customers in the U.K., Aspora plans to swiftly extend its reach to users in the United States and the United Arab Emirates (UAE). This geographical expansion is highly strategic, as the U.S. represents the largest source of inward remittances to India, accounting for nearly 28% of the total market share, according to India’s central bank. The UAE also hosts a significant Indian expatriate population, making it another critical market for Aspora’s growth. By targeting these key corridors, Aspora positions itself to capture a substantial share of the lucrative diaspora finance market.

Beyond Remittances: The Pursuit of "Stickiness"

A common challenge for fintech platforms in the remittance space is maintaining user engagement beyond sporadic transactions. Aspora’s CEO, Parth Garg, candidly acknowledged that the direct bill payment feature might lead to a marginal reduction in traditional remittances, estimating it at only 4% to 5% of total transfers. However, he articulated a strategic vision where the long-term benefits of increased user "stickiness" far outweigh this minor shift. "Today, the goal for any Neo bank is to try to get more and more transactions on your app," Garg explained. "With remittances, people used to use the app once or twice a month. Because of this new bill payment system, the new feature increases velocity on our platform and has our users visit the platform more frequently."

This analytical commentary highlights a broader trend in the fintech industry: moving from single-service providers to comprehensive financial ecosystems. By offering direct bill payments, Aspora transforms from a transactional money transfer service into an indispensable financial management tool for NRIs. The increased frequency of interaction fosters greater trust and loyalty, making users less likely to switch to competitors. This strategy not only secures existing customers but also opens avenues for cross-selling future financial products and services, such as the NRE (non-resident external) and NRO (non-resident ordinary) accounts that Aspora plans to launch next year. These accounts, designed to help NRIs manage foreign and Indian-earned income respectively, represent the next logical step in building a holistic financial platform catering specifically to the diaspora’s unique needs.

Market Momentum and Future Prospects

Aspora’s journey to this point has been marked by rapid growth and significant investor confidence. In June, the company successfully closed a Series B funding round, raising $50 million at a valuation of $500 million. This round was led by Sequoia, a venture capital giant renowned for backing successful technology companies, with participation from other notable investors including Greylock, Hummingbird, Quantum Light Ventures, and Y Combinator. To date, Aspora has secured over $99 million in total funding, a strong indication of its potential to disrupt and innovate within the cross-border payments sector.

The company’s impressive traction further validates its business model. Aspora has already amassed a customer base of 800,000, facilitating transactions totaling $4 billion and saving users an estimated $25 million in transfer fees. These figures underscore the significant value proposition Aspora offers, particularly its commitment to lower costs and improved efficiency compared to traditional financial channels. The successful testing of the new bill payment feature with thousands of users over several weeks, revealing mobile recharges as a particularly strong use case, provides further evidence of its market readiness and user demand.

The competitive landscape for diaspora-focused fintechs is increasingly vibrant, with numerous players vying for market share. However, Aspora’s integrated approach, combining competitive remittance services with direct bill payments and future plans for NRE/NRO accounts, positions it as a comprehensive financial partner rather than just a transaction facilitator. This holistic strategy, backed by substantial venture capital and a clear understanding of the NRI market’s evolving needs, sets Aspora apart.

In conclusion, Aspora’s introduction of direct bill payment capabilities for the Indian diaspora is more than just a new feature; it represents a significant leap forward in cross-border financial empowerment. By leveraging India’s advanced digital payment infrastructure and forging strategic partnerships, Aspora is not only simplifying complex financial tasks but also fostering deeper connections between NRIs and their families back home. This move is poised to enhance user engagement, reinforce Aspora’s position in the competitive fintech market, and ultimately contribute to a more efficient and interconnected global financial ecosystem. As Aspora continues to expand its services and geographical reach, it promises to reshape how millions manage their financial lives across continents.

{kind=link}